Unlock USDA Loan Benefits

Single Family Guaranteed

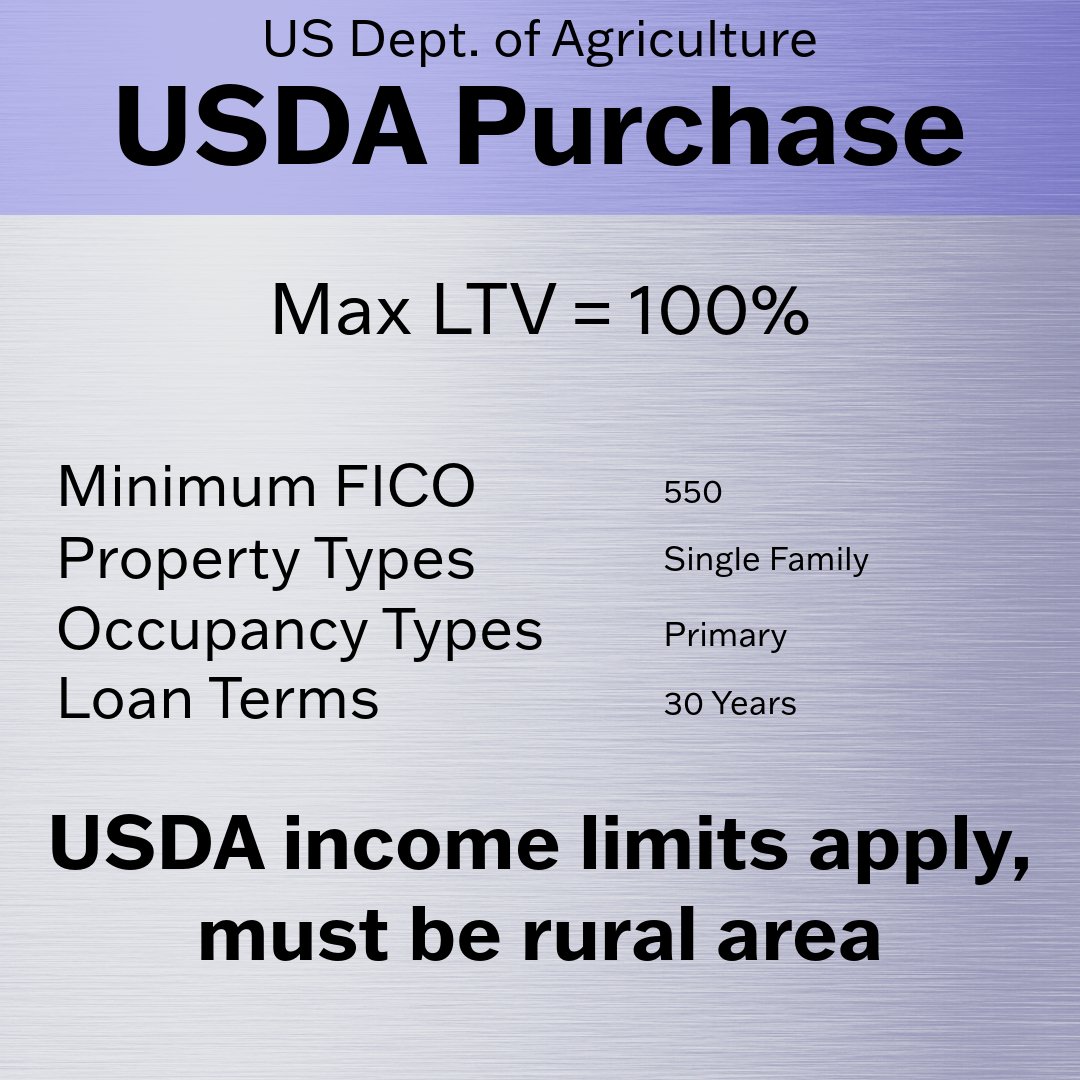

No Down Payment Required: Eligible borrowers have the opportunity to finance up to 100% of their home purchase price.

Competitive Interest Rates: Secure lower rates and mortgage insurance that make your dream home more affordable.

Eligible Rural Areas: The property must be a single-family residence in an approved rural location.

USDA Rehab Loan Option: Transform your property into your dream home with additional financing for renovations.

Streamline Refinancing: Simplify the process of lowering your monthly payments or shortening your loan term with USDA's Streamline refinance.